Production Linked Incentive (PLI) Scheme:Evaluation and The Way Forward

APRIL 2021

Satish Y. Deodhar

Professor, Economics Area, Indian Institute of Management Ahmedabad

Executive Summary

Announcement of the Production Linked Incentive (PLI) Scheme and its extensions in quick succession since April 2020 shows the will and urgency felt by the government of India to improve India’s competitiveness in the world market. The scheme envisages the government giving a subsidy of up to 4% to 6% of additional sales compared to the base year sales of a qualifying firm for a qualifying product. The total disbursement is expected to be close to ₹2 lakh crore over a 5 year period. Experience of the pre-liberalization period shows that schemes such as these are prone to suffer from long teeth-to-tail linkages and create potential for rent seeking activities. For Atmanirbhar Bharat, one needs generic policies that will enhance core competitiveness of the private sector without making it dependent on the state or cause regulatory capture. The elephant in the room is the inadequate state policies that can remove market imperfections, create public goods, improve state capacity and build institutions for skilling the work force. In this context, government may want to focus on power sector reforms, harmonization and downward revision of GST rates, managed float of the Indian rupee, competitive interest rates, spending on infrastructure that facilitates GVCs, tax incentives for R&D, skilling of factory work force through ITI-like training institutions and government bolstering domestic demand for defence and aerospace technology.

1. Introduction

The process of converting baser metals into gold was attempted by Alchemists centuries ago. The via media for this process was to somehow invent the philosopher’s stone. Even scientists like Robert Boyle and Isaac Newton were tempted to undertake this process but without success. Closer home in today’s times, Government of India would like to see substantial production growth in the technology sectors aiming for the goal of ‘make in India’ and ‘Atmanirbhar Bharat.’ In this context, the government’s Production Linked Incentive (PLI) Scheme announced in stages since April 2020 attempts to act like the proverbial philosopher’s stone. Notification of the PLI scheme for large scale electronics manufacturing (mobiles and electronic components) was issued in April and its detailed guidelines were announced by June (MeitY, 2020). Similarly, notification of PLI scheme for medical equipment was issued in July followed by its detailed guidelines in October (MCF, 2020). This process continued with the recent extension of the scheme to ten new sectors, which includes automobiles and auto components, advanced electrical batteries, pharmaceutical products, personal computers, laptops, air conditioners, telecom equipment and specified processed food products.

The sequential announcements of this scheme cast in stone did not catch the imagination of the print and electronic media. The announcements got shadowed by the passing of the farm bills in the parliament in September 2020 and the subsequent agitation in the nation’s capital to oppose these bills. In the current melee and clamour of the agitation however, one cannot ignore the ramifications of the PLI scheme. As of today, the total incentive expected to be disbursed on all the PLI sub-schemes would amount close to a whopping ₹2 lakh crore, i.e., ₹2 trillion or $27 billion in the coming five years (PIB, 2020). Such incentive, a euphemism for subsidy, is supposed to lower the cost for the firms. As identified in the PLI scheme notifications, absence of competitiveness of Indian products is on account of high cost of finance and power; unavailability of quality power; inadequacy of infrastructure, domestic supply chain and logistics; and limited capabilities in design, skills, and Research and Development (R&D).

2.Way the Scheme Works

Project Management Agency (PMA)

The essential idea of the PLI scheme is to give incentive to produce more. Of course, as a first step of the PLI scheme, a firm has to make an application. This application has to go to the particular ministry under which the firm’s industrial product falls. Surely, mere acknowledgement of receipt of application does not mean approval of the application. A nodal agency called Project Management Agency (PMA) is established for each ministry which will be responsible for providing secretarial, managerial and implementation support. However, the process is more cumbersome than what it promises. The PMA will carry out appraisal and verification of eligibility for support, examine claims for disbursement and compile data on progress and performance of incremental sales of manufactured goods over the period of the scheme. The incremental sales are defined as the difference between the sales in a particular year minus the sales in the base year of 2019-2020. If everything seems in order, the PMA will recommend to an Empowered Committee (EC), to give subsidy to the firm. A subsidy of 4% to 6% will be given each year on the incremental sales of the manufactured product, depending upon the nature of the industrial product and the year of eligibility during the 5-year period of the scheme.

Empowered Committee (EC)

Once PMA has recommended a list of firms, EC will consider their applications for approval. EC consists of the secretary from the concerned ministry where the application is made, secretary for economic affairs, secretary for expenditure, secretary for revenue, secretary of director general of foreign trade (DGFT) and CEO of NITI Aayog, no less. The EC is expected to conduct periodic reviews of eligible companies with respect to their additional investments, employment generation and production and value addition under the scheme. The EC may revise incentive rates, ceilings, target segments and eligibility criteria as deemed appropriate during the tenure of the scheme. The EC will also be authorized to carry out amendments to the scheme guidelines. Moreover, a technical committee (TC) may also be constituted to give recommendations on technical issues referred to by PMC and/or EC. Instituting TC is mentioned in the guidelines for PLI scheme for medical equipment. Finally, the sub-schemes cannot be rolled out unless the union cabinet approves the same.

Conditions

There are quite a few conditions imposed on the firms which the PMA and EC will scrutinize. The eligible firms could be domestic or foreign but must be registered manufacturing firms in India.

Depending upon the sub-schemes for different sectors and the specific industrial products therein, there are different minimum incremental sales requirements and minimum incremental and cumulative investment requirements that the firm has to make every year for being eligible for the incentive. The minimum requirements are different for domestic and foreign firms as well. Investments made in R&D are considered as incremental investments; however, a certificate from a statutory auditor has to be provided identifying the cost of technology, patents, copyrights and other intellectual property rights (IPRs). Incremental investments are expected to be of greenfield character. However, if new investments are made in the existing brownfield production facility, separate records are to be maintained for the same.

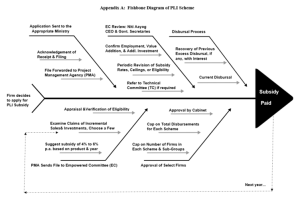

New plant and machinery must be used for the industrial products identified in the schemes. Spending on land and building including plant building however, is not considered for fulfilling the minimum requirement of incremental investment. After a lengthy scrutiny described above, if a large number of firms become eligible and government has to select a few, eligible firms will be arranged in the descending order of their global sales and a cut-off will be used to limit disbursal of incentive to a few. There is a cap on total disbursements in each sub-scheme and also on the number of firms that can qualify therein (Acharya, 2020). For example, only 5 firms each will be eligible for large size mobile phone firms and domestic mobile phone firms. The overall limit for medical equipment firms is 28 and within that a maximum of 10 firms will be selected from the sub-target segments. Then there are quite a few other conditions to be fulfilled including steep application fees, recovering excess disbursements from firms along with interest, etc. A typical administrative flow-chart of the PLI scheme is captured through a fishbone diagram in Appendix A.

3. Will the Alchemy Work?

Government’s attempt to create a new institutional policy structure for the PLI scheme, adding a host of norms, guidelines, rules and exceptions, throwing-in various sectors of the economy under its fold over time and then stirring and capping the incentive disbursements with the regulatory rod over the policy period can be a recipe for a heady concoction. It may not turn into a philosopher’s stone which can give a Midas’s touch to the lives of the citizens. While the upper echelons of policy making may have good intentions, one is not sure if the potential beneficiaries were consulted in drafting the policy. It always helps to choose some reputed firms with credibility to suggest a draft scheme that would be efficient, quick and simple to implement. Else, in many cases, deputies end up writing the detailed rules and regulations and the law of unintended consequences sets in. Therefore, the PLI scheme has to be viewed with scepticism. The detailed guidelines and rules of the scheme are such that rather than facilitating incentive for the deserving companies, they are focused more on preventing the undeserving entities from claiming the incentives (Mehta, and Kulkarni, 2020). In the process, the good firms may lose out.

In armed forces, there is a concept called teeth-to-tail ratio (Kelkar and Shah, 2019). For efficient delivery of supplies to the soldier at the border, this ratio has to be very low. It means, lesser the intermediaries the better. In the instant case, PLI application is to be made to an appropriate ministry. PMA constituted for that ministry will go through it and make recommendation to EC. EC will take a call but may consult TC. Once a decision is made, the file will go to competent authority for execution. That execution itself may take time. And, at each step, there is focus on documentation, reporting, enforcement and control. The teeth-to-tail ratio is, therefore, quite large in this scheme. To top it all, there are interest penalties on firms if excess disbursements are sanctioned for some reason. However, there are no penalties to the government for delays in processing and disbursements or insufficient disbursements of incentives (Mehta and Kulkarni, 2020). Thus, the guidelines are quite asymmetric. Creation of this mistrust between administration and business is not good for the success of the scheme.

As mentioned earlier, investments in land and building are not accepted for meeting the minimum investment requirement to get the PLI incentive. Money is a fungible asset and creating hurdles of this kind only dissuades firms from such schemes. For example, in the past, in the scheme for Mega Food Parks, investors were mandated to acquire multiple acres of land without government support. This had deterred interested parties from venturing in the food park projects (Mehta and Kulkarni, 2020). Disbursement conditions which require documentary proof of prior land holding make the life of potential entrepreneurs difficult. When government asks business persons to separate out greenfield investments on existing brownfield plants, the task is very complicated and goads firms to game the system. Moreover, when there is a cap on the total disbursement of funds in each sub-scheme as also the on the total number of firms that will be selected in different categories of products, it introduces lot of uncertainty among the applicants about their prospects. All told, the scheme incentivises significant discretionary element.

The proof of the pudding is in the eating. Already, many domestic firms as also foreign ones including Samsung and Apple’s contract manufacturers Wistron and Foxconn have approached the government to delay the starting of the first-year conditions on additional sales and investments. In their meetings with the senior officials from the Ministry of Electronics and Information Technology (MeitY), representatives of the firms have cited reasons for not starting new factories within the stipulated period. They have claimed that there have been inordinate delays in getting approvals for land acquisition deals. They are also claiming that there is an absence of adequately trained work force and that demand for their products is not likely to pick- up soon due to Covid-19 related slow-down. Based on the industry representation, officials from MeitY, PMA and EC including NITI Aayog CEO have been meeting among themselves but they are in no mood to alter the scheme conditions or deadlines of the initial schedule of 5 years. And despite these impediments, government has continued the process of extending the PLI scheme to a few more products such as laptops, iPads, all-in-one desktops and servers (TIE, 2021). One can only hope that these developments do not once again lead to rent-seeking activities of the pre- 1991 Licence-Raj era.

At a philosophical level, there always exists the problem of state capacity. It can arise due to wrong design of a policy and/or falling short in implementation (Kelkar and Shah, 2019). PIL scheme is a gargantuan scheme potentially costing 2 trillion over five years. It would need all the efficiency that the government can muster. Unfortunately, that is not easy to come by. In competitive markets, weak performing firms may exit the market and newer, more efficient ones may enter. In politics too, there is competition and politicians fear losing elections. That fear seems to make them attempt bringing-in positive changes. The nature of government agencies is such that they are monopolies in their field of activity and do not fear competition. When gargantuan schemes such as PLI are introduced, administrative structures get burdened and stretched and management of the scheme may pass from efficient to uninterested bureaucracy (Kelkar and Shah, 2019). Experience of the last many decades has shown that policies similar to the Licence- Quota-Subsidy Raj have had their unintended consequences–corruption, litigations, illegality and office/plant raids. In the process, ethical firms get dis-incentivised.

4. Why Choose Winners?

Government identifying industrial sectors for giving incentives and again choosing a few firms from each industrial sector amounts to selecting winners in a beauty contest. It does not become clear as to why the government would like to favour certain industrial sectors over the other (Acharya, 2020). Civil servants are extremely talented individuals, but they may not have the knowledge gained by risk-taking entrepreneurs in competitive markets. Regulators may even visit the plant sites, but may not be able to appreciate the nuances of incremental sales, investments and a blended source of production from greenfield and brownfield plants. Experience of many decades shows that businesses set up solely with the short-term motive to take advantage of the government largesse are prone to suspect accounting practices, procurement of shoddy equipment and poor sustainability (Ahluwalia, 2020).

In the past, government selecting small scale units (SSIs) for the production of certain goods has had unintended consequences. SSIs and village industries were selected for the production of toys in the early years of 1960s. It was hoped that this would remove the disadvantages faced by small firms. However, this was apparently done without studying the global toy industry or analysing local market conditions and pricing. It took many decades to correct this. China had become the toymaker of the world by then. The same story was repeated in the 1970s when the then upcoming TV industry was reserved for SSIs. The managing director of a European firm had commented clairvoyantly that government was licensing units for bankruptcy and that is what happened eventually (Mathur, 2020). When similar selection of SSIs was done for biscuits, large firms took a detour by having arm’s length contracts with SSI units but selling biscuits under their own brand. When electrical fixtures market was reserved for SSI, precision manufacturing of electrical fixtures was constrained and quality of fixtures suffered.

In choosing industry, firms and products for favourable treatment, the administration is likely to choose a dilettante, i.e., a gifted amateur. The administration may cultivate a genuine interest in the tasks thrust upon it by the policy decisions; however, it may not have real commitment or core competence to undertake the task. When Maruti Motors was hand-picked to produce the poor man’s car in the 1980s, prior to the launch, approval of a set of colours for the cars was taken up. While many board members suggested their colour preferences, Suzuki director declined to give his suggestion and wondered if there was any data on actual consumer preferences! The hint was enough and the firm conducted a survey among the potential customers (Mathur, 2020).

While the PLI scheme is in the process of selecting winners, one would also notice that the customs duties on imports of industrial products have been raised leading up to the announcement of the PLI scheme (Acharya, 2020). To give examples, duties on electronic and electric goods, watches, ceramics, glassware, toys and footwear have been raised to 20% and that on electric cars to 40% (Elara Capital, 2020). This move is in reverse of the phased reduction in customs duties that began with post 1991 economic liberalization in general and post WTO trade liberalization in particular. Protection to selected industries both through subsidies and customs duties can be a matter of concern. Such two-sided protection becomes difficult to remove later, for regulatory capture results in winners successfully lobbying for permanency of the protection. Reduction in competition would mean that the favoured firms will make higher profits and cronyism sets in (Aiyar, 2020). Moreover, it becomes that much harder for India to join any regional free trade agreements and compensate other countries for going against the norms set by WTO.

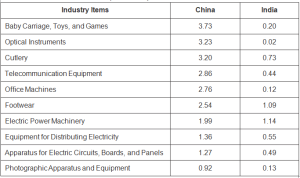

The PLI scheme was first introduced for mobiles and electronic components in April 2020. Later, medical equipment of various kinds were added and by the end of the year, the scheme was extended to ten more sectors which included items such as automobiles, computers, select processed food products, textiles, solar panels and more. The total outlay expected on the scheme is about 2 trillion in five years. But what stops leaders from the remaining industrial sectors to lobby for the PLI scheme? Or what stops the government from extending the scheme on its own to other products and sectors for political considerations? As reported in the previous section, the government is currently continuing the process of extending the PLI scheme to a few more products such as laptops, iPads, all-in-one desktops, and servers (TOI, 2021). Where will this stop? If the criterion has been to improve the competitiveness of Indian industry, then there are many more Indian products and industries which may not be competitive in the world market. Table 1 below shows the revealed comparative advantage (RCA) for sample products between China and India for the year 2019 (Elara capital, 2020).

A country is considered to have RCA for a given product if the ratio of her exports of that product to her total exports (X) exceeds the ratio of the world exports of that product to the world’s total exports (Y). If the RCA index, defined as X/Y is above 1 (RCA >1), it can be inferred that the country is a competitive producer of that product relative to a country producing and exporting that product at or below the world average. The higher the value of RCA, higher is the competitiveness of the country in that product. The RCA numbers in Table 1 for a sample of industry items show that China has strong competitiveness in diverse products like toys and games to footwear and cutlery. While India is competitive in footwear and electric power machinery, her competitiveness is much less compared to that of China. Similarly, although China does not have competitiveness in photographic apparatus and equipment, her performance is much better compared to that of India. In fact, if one were to compare these products with Vietnam, Vietnam’s competitiveness may be much higher than that of China in quite a few products. One could calculate such RCAs for all products as per the harmonized system (HS) of six-digit codes for many countries and do the comparisons.

Table 1: RCA in Sample Industry Items for China and India, 2019

One is not sure if such an exercise was done before implementation of PLI scheme. In any case, it is a good idea to keep a tab on knowing India’s RCAs – how far below they are from 1, for different industries and products. A comparison of such RCAs every three years across products and across countries will give a sense of direction of India’s competitiveness.

Even if India may have RCA higher than 1 for quite a few products not reported in Table 1 above, it could still be much lower compared to many other countries. Should those products and industries too be included in the PLI scheme? It is not clear if Indian government would give incentive through PLI scheme to those products where RCA is relatively high or relatively low. Of course, competitiveness or comparative advantage of a nation is a dynamic process which evolves over time. It will be impractical to keep adding and deleting products to the PLI scheme every now and then. Importantly, complex incentive schemes have dubious efficacy, they turn out to be distortionary and give scope for rent seeking behaviour and side payments to the intermediaries (Desai, 2020). Instead, what the country needs are generic policies of the government that create public goods and skilled workforce which increase productivity levels across the industrial sectors.

5. The Way Forward

What then is the way forward? Competitiveness of a nation is reflected in the level of national productivity. Higher productivity is reflected either in lower cost which make standardized commodities competitively priced in the world market or achieving sustained product differentiation which helps firms command premium prices and support high- wage skilled workers. The higher productivity in turn depends upon the national environment in which the local firms operate. Porter (1990, p. 72) has described four attributes of a nation and their mutually reinforcing spill-over effects through what he calls as the Diamond framework. The four attributes of this Diamond are, 1) Factor Conditions, which address nation’s position in factors of production such as say skilled labour and infrastructure required to compete in an industry; 2) Demand Conditions, which address the nature of home demand for the industry; 3) Related and Supporting Industries, which produce and supply critical components and complementary goods to a given industry; and 4) Firm Strategy, structure and rivalry, which address the conditions of how firms are created, organized, managed and compete with each other within the industry.

Porter does affirm that one of the important variables that can improve the performance of the Diamond framework is the government’s involvement and he is not talking about government’s direct intervention in selecting winners by giving subsidies/incentives and minimum support prices. If the incentives being offered through the PLI scheme are expected to subsidize the higher costs of the select industries and firms, it should be clear to us as to why the normal costs are high in the first place and would there be other direct ways of lowering the cost (Bhargava, 2020). The PLI scheme notifications themselves answer to the first question – India is not competitive because of high cost of finance and power; unavailability of quality power; inadequacies of infrastructure, domestic supply chain and logistics; and limited capabilities in design, skills, and Research and Development (R&D).

To lower such costs, instead of doling out scheme incentives worth about ₹2 lakh crore to select winning industries and firms, there is a wonderful opportunity for harmonization and downward revision the Goods and Services Tax (GST) structure for all industries (Ahluwalia, 2020). While most indirect taxes have been now lumped together under a single GST, there are still multiplicity of rates prevalent, ranging from 0, 5, 12,18, 28 and some with an additional cess. A blanket 10 percent GST rate will not only be abundantly efficient in terms of tax administration and marginal cost of tax collection, it will lower costs all across the Porter’s Diamond framework, making Indian industry more competitive. In the process, the goal of one nation, one tax, one registration and one rate (Kelkar, 2016) will be achieved.

Another low hanging fruit is the cost of electricity and its quality. If electricity is cheapest in China, India’s electricity is among the costliest in the world (Aiyar, 2020). Introducing reforms in the power sector would reduce cost and improve quality for all the stakeholders in the Porter’s Diamond, making Indian industries more competitive in the world market. While India initiated power sector reforms, its sequencing became problematic. Electricity generation was privatised first, leaving distribution companies (discoms) in the public sector. Due to the inefficiencies of the discoms, excess capacity was being wasted with the private power generation firms and paradoxically, power outages continued at the user end. Moreover, because the fuel market for generation of electricity was also controlled, private firms would get stranded for on-time fuel availability and fair price. Put together, a large amount of capital got blocked in new-age electricity generation plants (Kelkar and Shah, 2019; p. 251). To add to the woes, many states have continued to give free power to the farmers. This obviously has resulted in huge revenue losses to discoms.

These inefficiencies in the power sector get reflected in high cost of electricity and its poor quality. If the electricity reform is to be taken to its logical end, discoms all across India should be privatised first, fuel market next and then the generation plants. Importantly, privatization of the discoms has to be complemented by adoption of the Electricity Amendment Bill of 2020 which has proposed farmer subsidies to be replaced with direct benefit transfers (DBTs) to farmer bank accounts and set discom companies free from incurring losses. These reforms would usher in the required efficiency and lowering of electricity cost and as a result, inject cost competitiveness across the Diamond framework.

India is a country of continental proportions with significant presence of the non-tradable sector. Therefore, the nominal exchange rate of rupee does not necessarily change in tandem with the ratio of domestic and foreign inflation. In fact, in the last five years, the real effective exchange rate has remained overvalued for the Indian rupee. This would have certainly resulted in eroding the competiveness of Indian products abroad. To counter this, the government has been re- invoking protection through customs duties. In fact, as shown by Lerner (1936), a customs duty on imports is equivalent to imposing an export tax which reflects change in the relative prices of importables and exportables. Moreover, government is also selecting winners through PLI incentives which can have its unintended consequences. Instead, the government could offer a level playing field by depreciation of the effective real exchange rate by five to ten percent (Chhibber, 2020). RBI has adopted this ‘managed float’ policy in the past. It can achieve a few things in the process – improve competitiveness of Indian products and bolster the foreign exchange reserves for rainy days, which may now reach a sweet spot of $500 billion or more. Pursuing this managed float policy, particularly in the current times of recession would also be consistent with the expansionary monetary policy. Interest rates in India are generally higher than those in the rest of the world and expansionary monetary policy would help bring cost of capital down and make Indian industry more competitive in the world market.

Staying competitive is a dynamic process and it rests on ever increasing national productivity and innovations. While the above changes can be initiated in the short to medium term, a few other changes can be initiated in the medium to long term. For example, the factor conditions and related supporting industries of the Diamond framework can be bolstered in two ways – government enhances support to specialized researches into frontier technologies and basic research on the one hand and offers exemptions to private sector on long-term capital-gains tax, when ploughed-back new equity issues and greenfield projects are directed to cover R&D activities. Such exemptions to private sector could be tied to higher regulatory standards for product quality and environmental impact. When the higher regulatory standards eventually spread internationally, they give the nation’s companies a competitive edge. The Swedish government followed this policy and results showed – the Swedish firm Atlas Copco produced compressors that were much quieter than their competitors’ and were being used in crowded cities the world over (Porter, 1990; p. 648). As far as R&D in public institutions is concerned, rather than running only the stand-alone autonomous research institutions, government may promote R&D through competitive grants to universities. While the competitive grants encourage interdisciplinary research and funding of better projects, involvement of Ph.D. students from universities ensures cost competitiveness of R&D. Productivity is not just about R&D alone. It is also reflected in doing repetitive jobs quickly and doing them right. Therefore, skilling of labour force through ITI-like training institutions will improve work productivity in factory-level jobs (Deodhar, 2020).

The home demand factor of the Diamond framework too can be bolstered by government providing early demand in the defence and space industry for high-technology equipment, as has been done to the firms, Bharat Forge and Godrej Aerospace. Along with the long-term capital gains tax exemption for R&D, this would give a push to the competitiveness of domestic industry through demand certainty, economies of scale, and innovations. Needless to say, demand creation of this kind also goes a long way to strengthen national security. Another boost to the home demand that government can give, especially in the depression-like conditions of today, is to focus on massive physical infrastructure projects like roads, railways and ports. Such infrastructure support will facilitate mobility of finished goods, raw material and labour, increasing the efficiency and competitiveness of the Indian products. Recently, one of the co-founders of the Indian cell phone and electronics firm Micromax mentioned that the average speed of trucks on Indian roads is not more than 45 km to 50 km per hour and it takes days for a truck to transport goods from one end of the country to the other, despite replacement of border taxes of state governments with GST. This is in stark contrast to speedy movement of goods on the huge road infrastructure China created more than 2 decades ago.

Moreover, as far as private foreign direct investment (FDI) is concerned, it could be directed not just for manufacturing but for the global value chain (GVC) pipeline which will also lead to efficient movement of goods and factors of production. Dhavan and Sengupta (2020) have identified vehicles, vehicle components, capital goods, machine tools, and pharmaceuticals as India’s mature and skill intensive value chains which have proven sophisticated capability both in domestic and export markets. Food and agriculture, apparel and textile, leather, rubber, furniture, metals, and basic material are categorised as raw material intensive value chains mostly serving domestic market. Electronics, semiconductors and renewable energy are identified as technology driven emerging value chains. Aerospace and defence are defined as technology driven value chains but operating only in the domestic market. All these GVCs can be accelerated if capacity at local, state and central government level is enhanced in terms of single window regulatory approvals, increased use of digital and rule-based compliance, speedy logistics, and competitive rates for power and credit. Finally, government must continue to follow anti-trust policies to create healthy completion among firms, which may result in product innovations and competitiveness vis-a-viz the rest of the world.

6. Concluding Comments

Announcing of the PLI scheme and its extensions in quick succession shows the will and urgency felt by the government of India to improve India’s competitiveness in the world market. The scheme envisages government giving a subsidy of up to 4% to 6% of additional sales compared to the base year sales of a qualifying firm for a qualifying product. The total disbursement is expected to be close to ₹2 lakh crore over a 5 year period. The description of the scheme given in earlier sections and its X-ray in the fishbone diagram (Appendix A) however, remind one of the inordinate administrative processes followed during the pre-liberalization era. What began as a PLI scheme for mobiles and electronic components in April 2020 was extended over time to medical equipment and later to quite a few other products including those from the food processing sector. Recently, leaders of electronics industry have met the government officials for delaying and roll-over of the scheme’s first-year deadlines on additional sales and investment requirements. The firms are finding it tough to strike land acquisition deals for starting new factories within the stipulated time and also experiencing shortage of skilled work force. Despite such impediments, government is continuing to extend the scheme to newer items such as laptops, iPads, and servers (TIE, 2021).

Such instances are reminders that government schemes directed at specific products or sectors suffer from too long teeth-to-tail linkages, limitations of the state capacity, and the resultant potential for rent seeking activities. As discussed in the earlier sections, we need policies that are neutral to industry stakeholders and not make industries directly dependent on state or cause regulatory capture. The state policies should result in cost reduction and productivity gains across industrial sectors that act as force multipliers for Indian industry to become competitive world- wide. The elephant in the room is the inadequacy of generic state policies that can remove market imperfections, create public goods, improve state capacity and build institutions for skilling the work force. In this context, power sector reforms, harmonization and downward revision of GST rates, managed float of the Indian rupee, competitive interest rates, spending on infrastructure that facilitates GVCs, tax incentives for R&D, skilling of factory work force through ITI-like training institutions and government bolstering domestic demand for defence and aerospace technology are some of the measures that the government may adopt to increase India’s competitiveness in the world market.

Porter affirms that such indirect state policies reinforce competitiveness among the interlinked sectors of the Diamond framework. For Atmanirbhar Bharat, one needs generic policies that will enhance core competitiveness of the private sector. In contrast, the processes involved in the PLI scheme may turn out to be the alchemy trying to seek the enigmatic philosopher’s stone. One needs to adopt modern chemistry.

7. References

Acharya, S. (2020). A subsidy-tariff-permit raj?: If each PLI scheme is to be run by different ministries it’s easy to envisage a hydra-headed bureaucracy, Business Standard, November 26, accessed on 4/1/2021 from https://www.business-standard.com/article/opinion/a-subsidy- tariff-permit-raj-120112600047_1.html

Ahluwalia, S. (2020). Marching alone, Opinion India, Times of India, November 20, accessed on 5/1/2021 from https://timesofindia.indiatimes.com/blogs/opinion-india/marching- alone/?source=app&frmapp=yes

Aiyar, S. (2020). India isn’t China. Copying its industrial, trade policy could invite sanctions, Swaminomics, Times of India, November 15 , accessed on 4 / 1 / 2021 f rom https://timesofindia.indiatimes.com/blogs/Swaminomics/india-isnt-china-copying-its- industrial-trade-policy-could-invite-sanctions/?source=app&frmapp=yes

Bhargava, R. (2020). E-Mail Communication, November 23, in reply to article by Mehta and Kulkarni (2020).

Chhibber, A. (2020). PLI signals the recognition that laissez-faire won’t work in a fiercely competitive global market, Economic Times, November 30, accessed on 6/1/2020 from https://economictimes.indiatimes.com/news/economy/policy/view-pli-signals-the-recognition- that-laissez-faire-wont-work-in-a-fiercely-competitive-global-market/ articlesh ow/79497055.cms?from=mdr

Deodhar, S. (2020). “Make in India: Success Stories, Lessons Learnt,” in Indian Economy: The Great Slowdown? Uma Kapila, ed., New Delhi: Academic Foundation.

Desai, M. (2020). E-Mail Communication, November 20, in reply to article by Mehta and Kulkarni (2020).

Dhawan, R. and Sengupta, S. (2020). A new growth formula for manufacturing in India, McKinsey & Company, October 20, accessed from https://www.mckinsey.com/industries/advanced- electronics/our-insights/a-new-growth-formula-for-manufacturing-in-india, on 17/2/2021

Elara Capital (2020.). “India’s Manufacturing Moment,” Economics, Elara Capital, Elara Securities (India) Private Limited, November 9.

Kelkar, V. (2016). Fiscal Reforms in Federal Framework, The Shankar Aiyar Memorial Lecture, October 21, Chennai

Kelkar, V. and Shah, A. (2019). In Service of the Republic: The Art and Science of Public Policy, Gurgaon, India: Penguin Random House.

Lerner, A. (1936). The Symmetry Between Import and Export Taxes, Economics, New Series, Vol 3 (11), August, pp. 306-313,

Mathur, V. (2020). E-Mail Communication, November 24, in reply to article by Mehta and Kulkarni (2020).

MCF (2020). “Guidelines for the Production Linked Incentive (PLI) Scheme for Promoting Domestic Manufacturing of Medical Devices,” Ministry of Chemicals and Fertilizers (MCF), Department of Pharmaceuticals, Government of India, October 29, accessed on 3/1/2021 from h t t p s : / / p h a r m a c e u t i c a l s . g o v . i n / s i t e s / d e f a u l t / f i l e s / R E V I S E D E % 2 0 G U I D ELINES%20FOR%20MEDICAL%20DEVICES%2029-10-2020_0.pdf

Mehta, P. and Kulkarni, A. (2020). The difficulty of decoding business incentive schemes, Live Mint, November 19, accessed on 4/1/2021 from https://bit.ly/38Zk8xx

MeitY (2020). “Guidelines for the Operation of Production Linked Incentive (PLI) Scheme for Large Scale Electronics Manufacturing,” Ministry of Electronics and Information Technology, June 1, accessed on 3/1/2021 from https://www.meity.gov.in/writeread data/files/PLI-Guidelines- 01062020.pdf

PIB(2020). “Cabinet approves PLI Scheme to 10 key Sectors for Enhancing India’s Manufacturing Capabilities and Enhancing Exports – Atmanirbhar Bharat,” Press Information Bureau (PIB), G o v e r n m e n t o f I n d i a ( G O I ) , N o v e m b e r 11 , a c c e s s e d o n 3 / 1 / 2 0 21 f r o m https://pib.gov.in/PressReleasePage.aspx?PRID=1671912

Porter, M (1990). “The Competitive Advantage of Nations,” Harvard Business Review, March-April.

TIE (2021). IT Min Rejects Demands, not to Extend First Year PLI Deadline, Economy, The Indian Express (TIE), February 23, Ahmedabad Edition.

8. Appendix A: Fishbone Diagram of PLI Scheme